Liquidity, currency

Inflation remains low

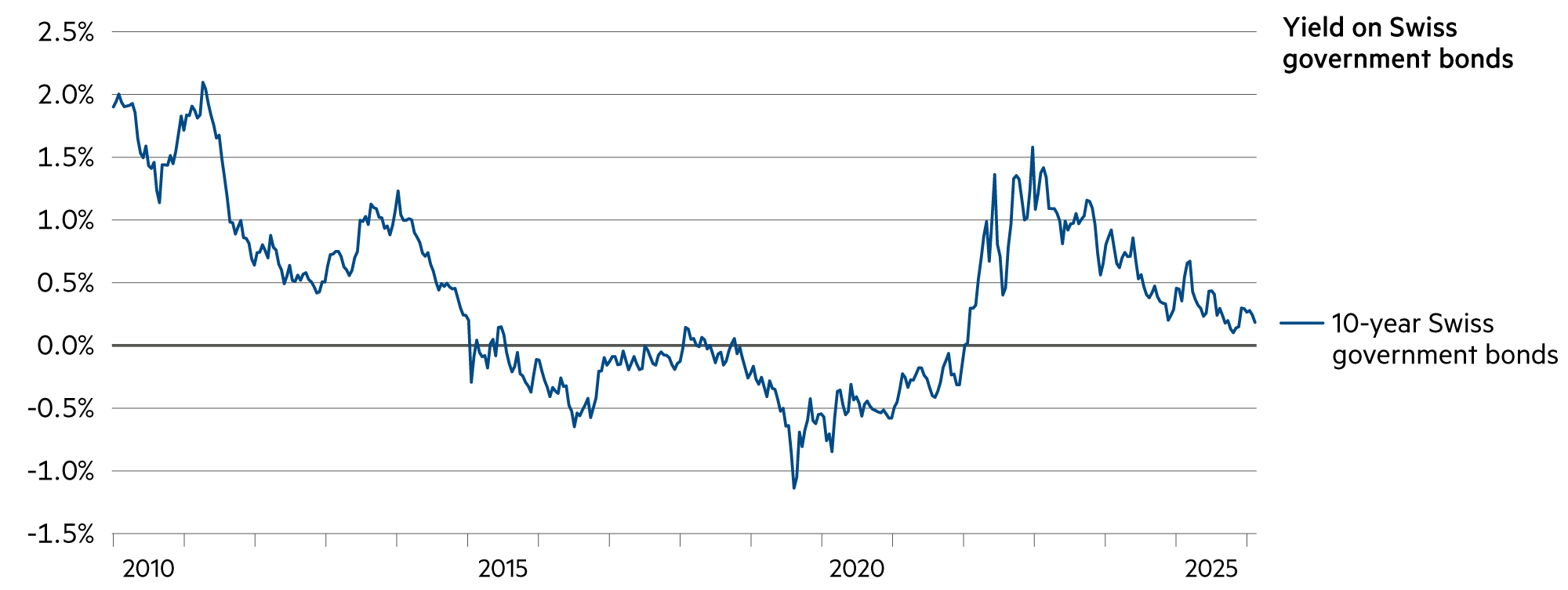

The Swiss franc remains a strong currency. Inflation is practically zero, which is why the Swiss National Bank’s monetary policy assessment in three weeks’ time is unlikely to give rise to any change in the key interest rate of 0%. The appreciation against the dollar and the euro in the first two months is now likely to give way to a period of stability lasting several months.

Read more Close

Fundamentally, the dollar’s appeal as a safe haven is waning as US stocks appear riskier while stocks in other countries are improving. This is another observation from last year that continued in the first two months of 2026. A less attractive US currency increases the incentive for global investors to reduce their dollar exposure.

This was the case during the tech bubble at the turn of the century. It is entirely possible that the dollar will fall again if stock prices decline, just as it did during the dot-com phase in 2002 when stocks performed better elsewhere. At that time, however, there was also a series of negative stock market news from the US. Today, on the other hand, technological leadership in various fields remains unbroken, and sales and profit figures are rising rapidly.

The US stock market’s focus on AI and AI-related cannibalization risks are weighing on the US, while loose fiscal policy is benefiting stocks in the rest of the world. Nevertheless, the high costs of currency hedging are being dispensed with in many places. Over the past 12 months, average currency hedging costs have been above 4% (franc vs. dollar). It is quite possible that they will fall below 4% in the next 12 months, but they will certainly remain substantial.

The decision to increase hedging ratios is independent of more general geopolitical considerations that could lead to diversification away from the US currency. Some analysts maintain their pessimistic assessment of the dollar, as the currency may have lost its special status in terms of yield, growth, and security. In Europe, there are even dreams of digital sovereignty.

We are not guided by dreams, nor do we engage in fictional scenarios such as those recently circulated by Citrini Research. Market confidence may be fragile, and fears of AI disruption may still turn into widespread risk aversion in many industries.

However, the fact remains that the technological dominance of US companies such as Microsoft, Google, Amazon, Nvidia, and AMD is based on decades of investment in innovation – and on the ability to retain innovative and (highly) qualified employees with generous compensation packages. This can even be seen in high-wage Switzerland, where around 10,000 employees work for US tech companies, 6,000 of them for Google in Zurich alone – most of them with university degrees.

| Asset class | 3–6 months | 12–24 months | Analysis |

|---|---|---|---|

| Bank account |

|

|

The SARON swap rates, which are important in banking, are all negative in the range from one month to three years, mostly around -0.1%. |

| Euro / Swiss franc |

|

|

Over the past 12 months, the EUR/CHF exchange rate has fallen by around 3%. Most recently, the euro was trading at 0.91 francs with minor fluctuations. |

| US dollar / Swiss franc |

|

|

At the beginning of March, the dollar rose by around 1% due to the crisis in the Middle East. This is in line with the SNB's monetary policy objectives. |

| Euro / US dollar |

|

|

At the end of February, the EUR/USD stood at 1.18, virtually unchanged from the start of the year. The war in Iran is likely to strengthen the dollar (temporarily). |