Liquidity, currency

Stability of the Swiss Franc

We continue to expect the franc to remain stable. Although the Swiss National Bank’s (SNB) conditional inflation forecast for the coming quarters is slightly higher than in December due to rising energy prices, medium-term inflationary pressures have hardly changed since the last economic assessment. Monetary policy is helping to keep inflation within the price stability range and is supporting economic development.

Read more Close

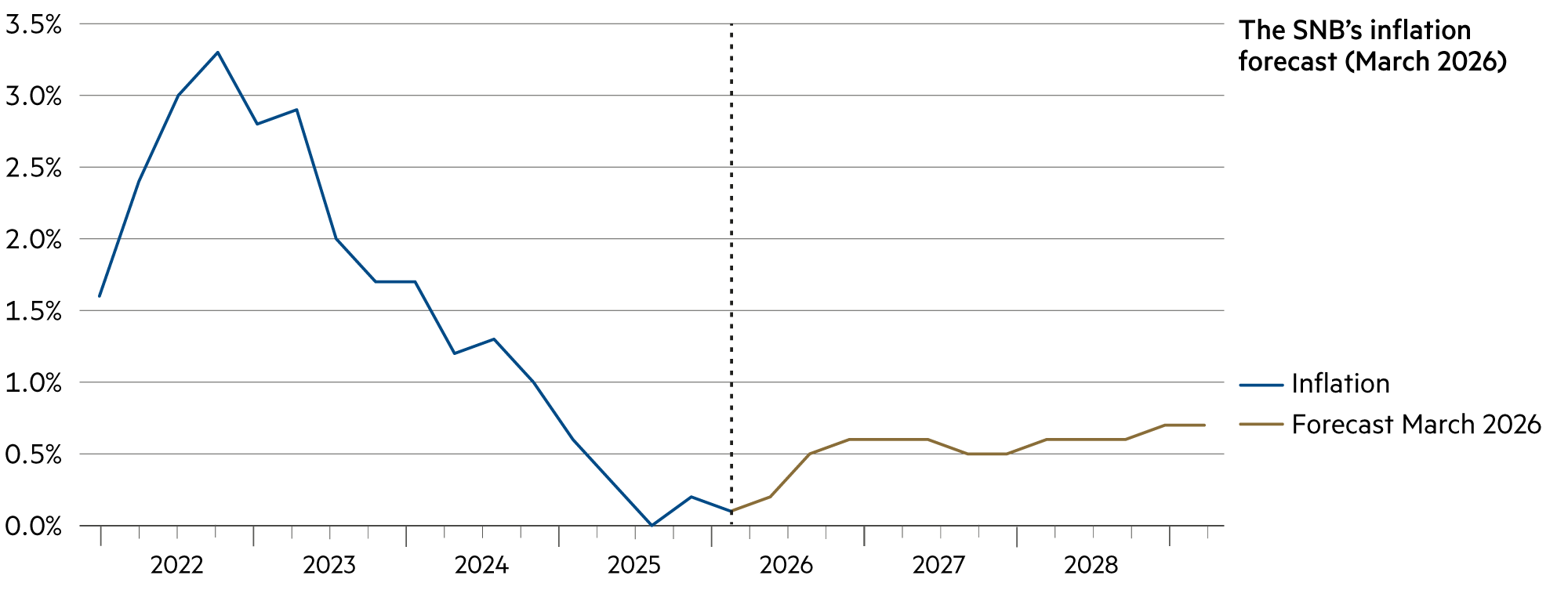

The National Bank will continue to monitor the situation closely and adjust monetary policy if necessary to ensure price stability in the medium term. As expected, inflation has risen slightly since the SNB’s last assessment of the economic situation, from 0.0% in November 2025 to 0.3% in March 2026 (Y-o-Y). Higher commodity prices have contributed in particular to this increase.

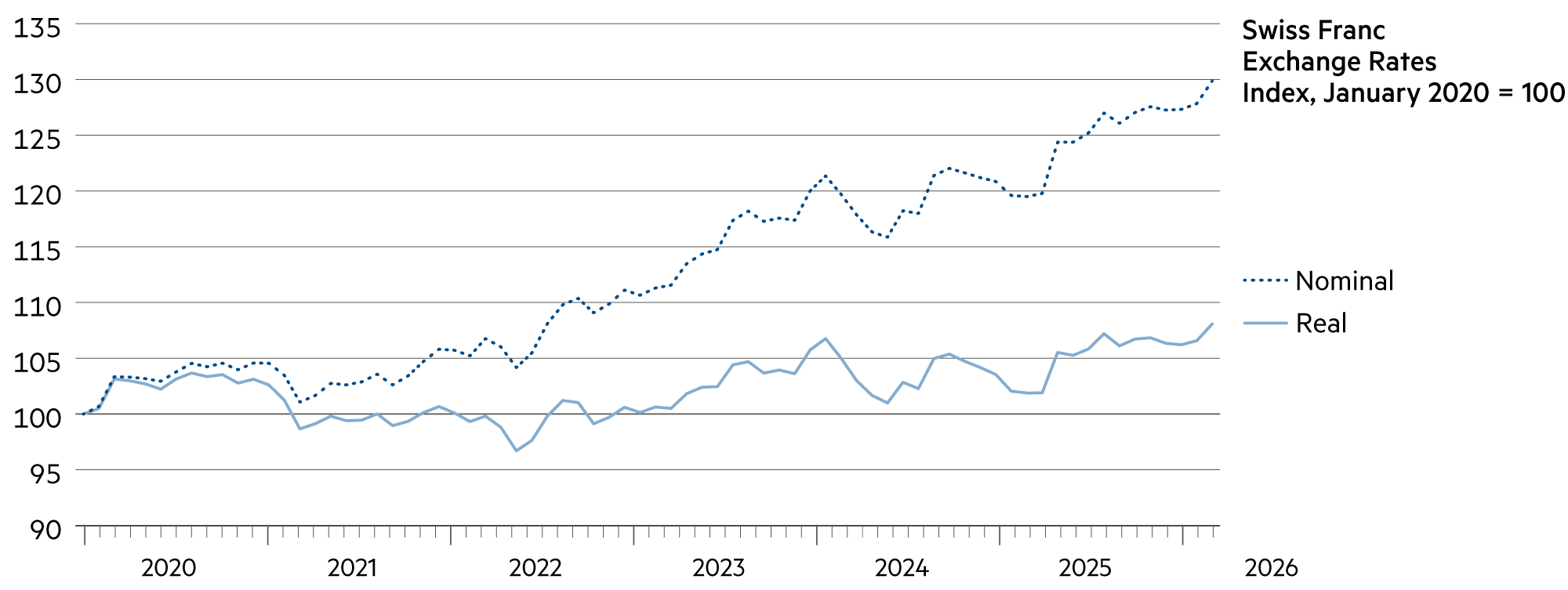

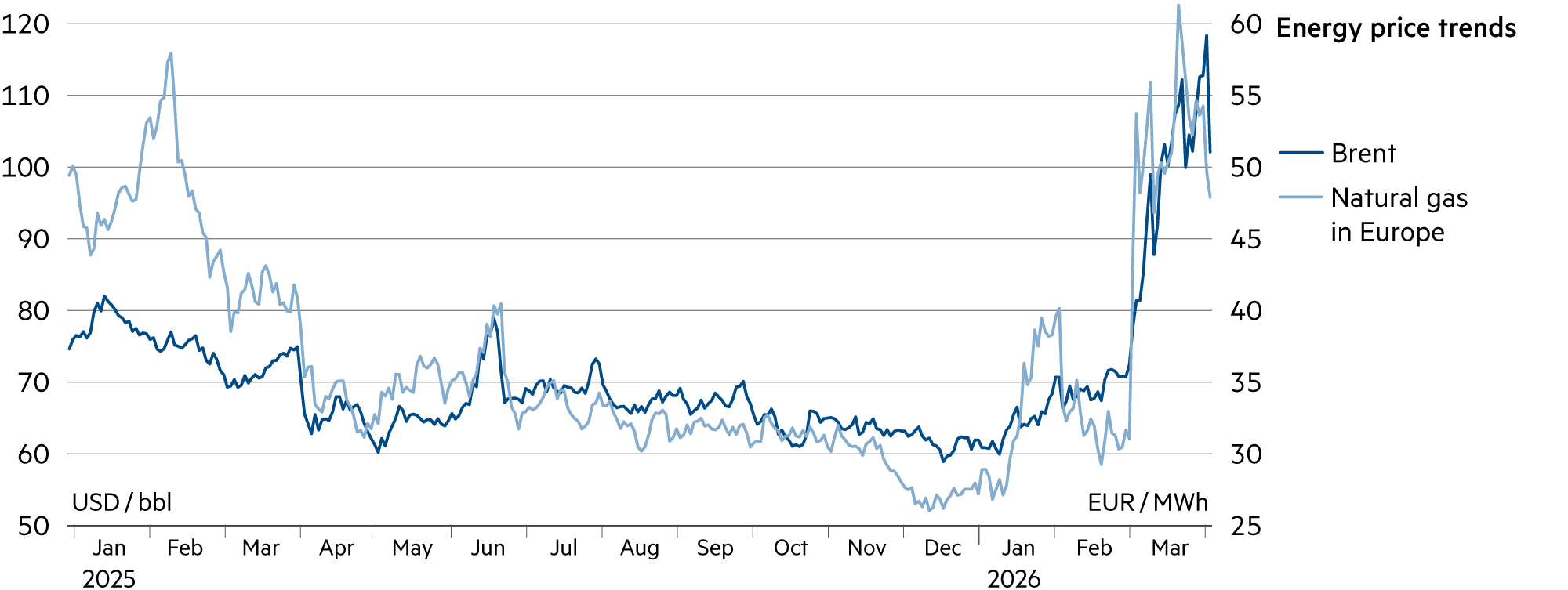

With energy prices rising due to the escalation in the Middle East, inflation is likely to increase more sharply in the coming quarters, though the stronger Swiss franc will counteract this in the medium term. On a trade-weighted basis, the Swiss franc has appreciated by around 2.5% since mid-December. Consequently, the SNB forecasts annual average inflation rates of 0.5% (2026 and 2027) and 0.6% (2028).

This is a far cry from the inflation spike of 2022 and 2023, which was temporarily associated with inflation rates exceeding 3%. The annual average inflation rate in 2022 was 2.8%.

Because interest rates in Switzerland are significantly lower than abroad, this makes investments in Swiss francs less attractive to foreign investors and thus counteracts upward pressure on the currency. The stimulative effect of low interest rates is also evident in the robust growth of credit in Switzerland. In this way, the SNB’s monetary policy supports economic development.

Conversely, franc investors who invest their capital abroad face the question of whether at least part of this exposure should be hedged. Hedging costs against the dollar stood at around 3.9% annually at the end of March, and around 2.3% against the euro.

Ultimately, the franc’s appreciation is largely driven by the inflation differential. It makes imports cheaper. If these imports are processed into higher-value goods through corresponding productivity improvements, the Swiss economy can tolerate the resulting increase in export prices. A moderate appreciation of around 2% to 3% per year is like a constant fitness regimen for local companies. They must constantly and continuously improve in order not to lose international competitiveness.

Moreover, the SNB rightly emphasizes that stable and favorable economic conditions – including price stability – are more important today than ever. Price stability is a key prerequisite for growth and prosperity in Switzerland. Stable prices provide planning certainty and thus facilitate purchasing and investment decisions. Stable prices benefit everyone, but they particularly protect lower-income households, which are most vulnerable to losses in purchasing power caused by inflation – that is, by (sharp) rises in consumer prices.

| Asset class | 3–6 months | 12–24 months | Analysis |

|---|---|---|---|

| Bank account |

|

|

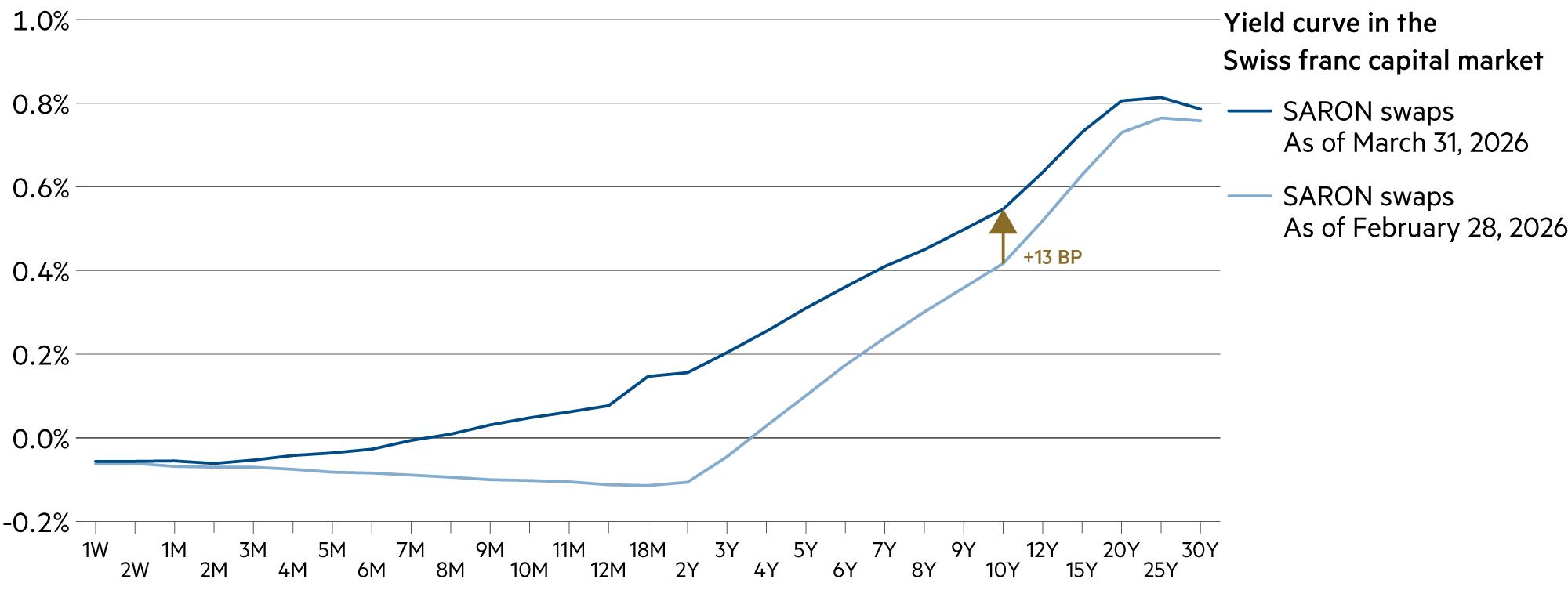

SARON swap rates are slightly negative in the short-term segment (up to 6-month maturity). In contrast, 10-year bonds are yielding +0.3%. |

| Euro / Swiss franc |

|

|

Rising yields in the eurozone drew investors back to the euro. The EUR/CHF exchange rate rose in March from 0.90 (March 6) to 0.92 (March 31). |

| US dollar / Swiss franc |

|

|

The trend toward easing in US interest rates has come to a halt. This strengthened the dollar. The USD/CHF exchange rate rose from 0.77 at the end of February to 0.80 (March 31). |

| Euro / US dollar |

|

|

With the EUR/USD exchange rate at 1.15, the market has stabilized. Real growth rates across the economic regions are expected to converge in the coming period. |