Liquidity, currency

Stability of the cost of living

In times of rising energy prices, many households face the challenge of stabilizing their cost of living without making significant cutbacks. In the U.S. economy, approximately 12.5% of household spending is currently spent at gas stations. Recently, this share was still at 7%. An increase in spending in one area tends to lead to savings in other areas—unless the savings rate is temporarily reduced or the number of hours worked is increased.

Read more Close

Household liquidity depends on one key factor: the number of hours worked, which is ultimately the decisive determinant of household income. If the number of aggregate (gainful) working hours increases, this leads to additional consumption and, ultimately, to growing gross domestic product (GDP).

GDP growth can also be boosted by an increase in labor productivity, which ultimately leads to higher hourly wages over the long term. According to OECD analyses, it is primarily large companies that exhibit above-average productivity growth. This is likely due in many cases to product and process innovations. In addition, large companies benefit more from economies of scale and network effects and can, for example, better spread costs incurred to meet regulatory requirements across larger sales volumes.

As we also observe in the capital markets, larger companies typically exhibit greater profit resilience: due to their market position, they can either better absorb or pass on higher costs. This was already evident during the COVID-19 pandemic.

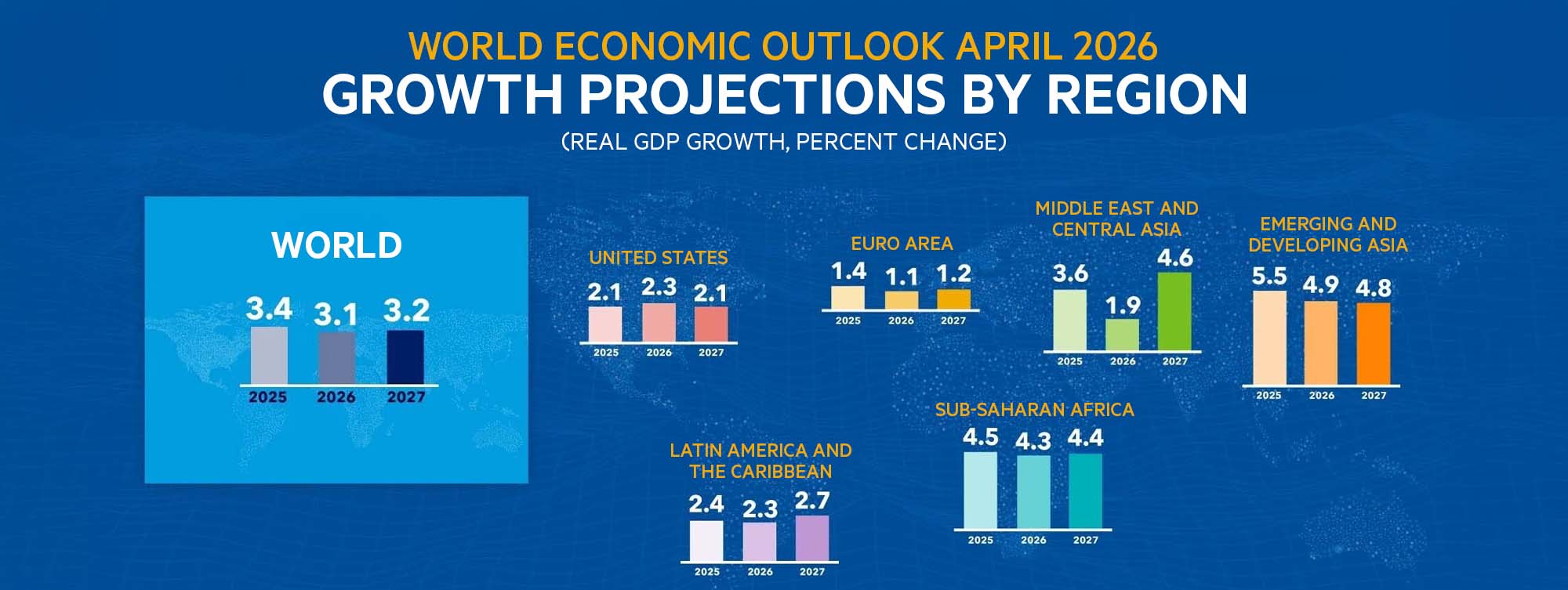

The global economy faces numerous challenges. Yet fears of stagflation seem exaggerated to us. Rather, we are observing robust revenue and profit growth. This is particularly pronounced in the technology sector, where investment plans for cloud and AI have recently been ramped up. Currently, the sustainability of profits across the entire economic cycle is being reassessed. Energy-related input costs account for only a small portion of the rapidly expanding revenues for cloud services.

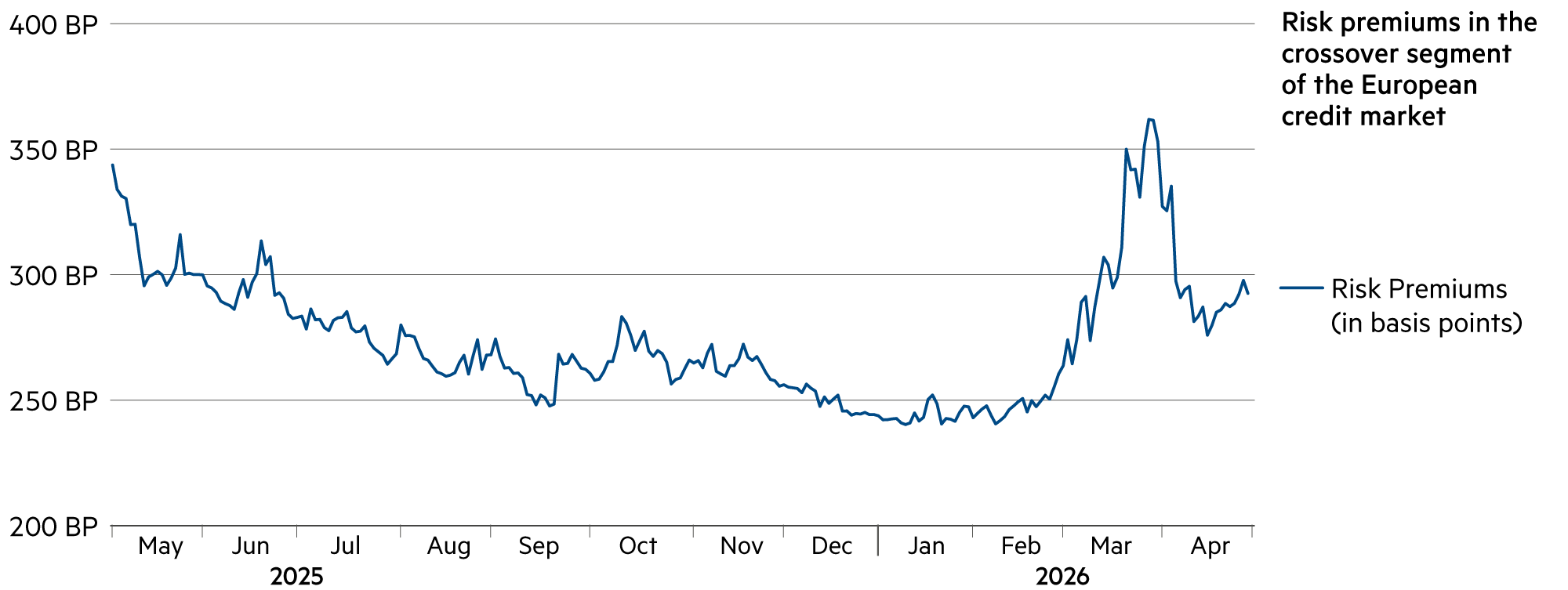

Credit markets react sensitively to fundamental changes in the capital markets. Yet since the start of the year, they have remained resilient, suggesting that the recalibration of power dynamics in the Middle East is not viewed as fundamentally “earth-shattering.” Credit spreads, which widened amid heightened risks of escalation, have already narrowed again, indicating reduced stress, even though central banks have not responded by easing monetary policy. The strength of the U.S. dollar is in line with expectations but is likely to ease again once tensions subside.

| Asset class | 3–6 months | 12–24 months | Analysis |

|---|---|---|---|

| Bank account |

|

|

SARON swap rates remain slightly negative for maturities up to 6 months. 10-year swap rates, on the other hand, stand at +0.6%. |

| Euro / Swiss franc |

|

|

At 0.92, the euro is showing its strength even at the start of May, as the ECB has so far detected “no second-round effects” in inflation trends. |

| US dollar / Swiss franc |

|

|

At 0.79, the USD/CHF exchange rate is about 1% lower at the start of May than at the beginning of the year, though fluctuations are more pronounced than with the euro. |

| Euro / US dollar |

|

|

At 1.17, the EUR/USD exchange rate is back at exactly the same level at the start of May as it was at the beginning of the year. |